A few days ago, I mentioned a credit builder loan. I want to explain more about it now.

A few days ago, I mentioned a credit builder loan. I want to explain more about it now.

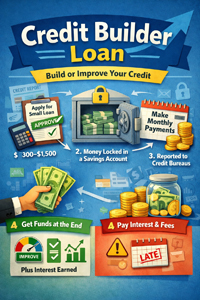

Credit builder loans are intended for people who need to build or rebuild their credit. People used them when they have very little credit histories or need to recover from mistakes in the past. It’s different from traditional loans. It’s meant to show that you can borrow money responsibly.

When you take out one of these loans, the lender will normally approve you for a loan of between $300-$1,500. Instead of giving you the money up front, the lender will put those funds into a secured savings account or a certificate of deposit. You will then make payments to “repay” the loan over a period of time, usually 6 to 24 months.

Assuming the payments are on-time, the lender will report your payments to the 3 major credit bureaus. This helps you build a good payment history which is the most important factor in your credit score. Once the loan is “paid off,” the lender will return the amount in the CD or savings account to you with any accrued interest it has earned.

Will you have to pay interest on this loan? Absolutely. And, if you miss a payment, you could incur a small fee. Additionally, missed payments will hurt your credit, not help so you need to ensure that any loan of this type that you take, you can afford the payments. It’s also recommended you set up automatic payments to make sure the payments are made on time. Remember, you’re paying this loan back out of pocket, not with the deposited funds. Those funds can be considered collateral for the loan.

Moral of the story:

Consider a credit builder loan for rebuilding credit, a starting point if you’ve never had credit before, or as an alternative for a credit card. If you use them judiciously, and with good financial behaviors, they can be a low-risk, steady step towards building good credit and financial assurance.