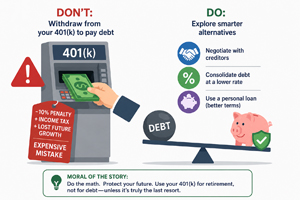

Withdrawing from a 401(k) to pay off debt is tempting, quick cash, instant relief, and instant regret. Before you turn your retirement into a one-way ATM, remember that withdrawals before age 59½ typically incur a 10% early withdrawal penalty plus ordinary income tax on the distribution. That $10,000 withdrawal can become a $2,500–$4,000 or more lesson in “don’t do this,” depending on your tax bracket. Worse, you also lose future tax-advantaged growth, compound interest is like a snowball. Take away the snow and you’re stuck with a pebble, potentially costing you tens or hundreds of thousands over decades.

Withdrawing from a 401(k) to pay off debt is tempting, quick cash, instant relief, and instant regret. Before you turn your retirement into a one-way ATM, remember that withdrawals before age 59½ typically incur a 10% early withdrawal penalty plus ordinary income tax on the distribution. That $10,000 withdrawal can become a $2,500–$4,000 or more lesson in “don’t do this,” depending on your tax bracket. Worse, you also lose future tax-advantaged growth, compound interest is like a snowball. Take away the snow and you’re stuck with a pebble, potentially costing you tens or hundreds of thousands over decades.

There are narrower situations where tapping retirement savings can make sense. If you’re drowning in extremely high-interest debt (e.g., payday loans) and no other floatation devices, or if your plan lets you take a 401(k) loan instead of a distribution (I don’t recommend option B). A loan avoids taxes and penalties and you’re basically repaying yourself back with interest. It’s like lending money to your future self who actually pays you. BUT it reduces your investable balance and can trigger full repayment if you leave your job.

A safer alternative is negotiating with creditors, consolidating debt at a lower interest rate, or using a personal loan or home equity line if terms are better than the tax/penalty hit (don’t like this last one as it puts your home at risk). Run the numbers: compare total cost of withdrawal (taxes + penalty + lost future growth) versus interest savings from paying the debt. Don’t forget emergency savings. Depleting retirement funds for debt is like fixing a leaky roof by selling the ladder.

Moral of the story:

If you’re overwhelmed, consult a fee-only financial planner or certified credit counselor for tailored options. Avoid withdrawing from your 401(k) for debt repayment unless you’ve exhausted other affordable options and the math, not just panic, proves it’s worth the hit.